Money & Investing Blog

BeManaged March ’10 Newsletter – The Advancing US Dollar and Your 401(k)

The following are some of the topics discussed in this month’s newsletter from John Whaley, CFA, AIF, the Director of our Research Department.

Advancing US Dollar Translates to Declining Foreign Stock Returns

Mutual Fund Fees and the Impact on Your Acccount

How Does Your 401(k) Account Growth Compare?

Brokers Win, Investors Lose Key Reform – WSJ

Every investor working with a financial planner/wealth manager/financial advisor/stockbroker…whatever title is used…should read at least the following quote. In Jason Zwieg’s article on WSJ.com, he provides one of the easiest to understand summaries I have read on the responsibility that person has to you:

As of now, the roughly 630,000 brokers, bankers and insurance agents registered to sell securities must determine whether investments are “suitable”—based on how wealthy you are, what else you have invested in, your tax status and your investment objectives.

Securities salespeople generally aren’t obligated to act in your best interest. They needn’t tell you that they make extra money pushing one particular investment or that cheaper alternatives might provide you a higher return.

Suppose two mutual funds are “suitable,” but one of them pays the broker a fatter fee. You may well end up in that one—without finding out that your broker had an incentive to favor it.

On the other hand, financial advisers—who are regulated as “fiduciaries” under the federal Investment Advisers Act—are obligated to put you first. They must explain their fees, disclose conflicts of interest and disclose past infractions. If they get paid extra to recommend a fund or sell an insurance product, they have to tell you.

Read MoreNew 401(k) Advice Proposal Available for Comments Until May 5th

As promised, the new 401(k) advice proposal has been delivered before the end of the month. While I admit to not having read it in its entirety, the following has been reported by the Wall Street Journal:

Read MoreStudies Show the Less You Do With Your 401(k), the More You Earn

ometimes, it helps to hear this from an independent source…

Don’t take this too personally, but the less you are involved with investment decisions for your 401(k) the better off you may be.

Sometimes, it helps to hear this type of thing from an independent source. As we have said before, we don’t fix our own cars, why should we be expected to be professional investment managers?

Don’t take this too personally, but the less you are involved with investment decisions for your 401(k) the better off you may be.

A new study of more than 400,000 401(k) participants in seven corporate plans found that the median return earned by individuals who sought out help in managing their 401(k) was 1.86 percentage points more than participants who made their own allocation/investment decisions.

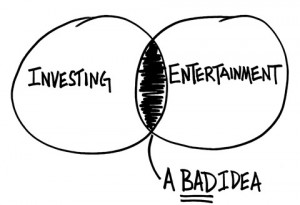

Read MoreInvesting Is Not Entertainment

As you know, we are big fans of the BehaviorGap. Our friend Carl Richards is now being featured in the New York Times website. His latest post there is two minutes of really good advice.

Am I investing to meet my most important financial goals or am I investing as a form of entertainment? For almost all of us, it can’t be both.

Video: Quick and Easy 401(k) Moves

We are a fan of keeping things simple, so when we run across tips on how to do so, we like to make sure we share them with you. The following video is an example of such tips; this one specific to your 401(k) plan.

There is one thing we would like to add to the idea of consolidating your old 401(k)s: If your company has BeManaged available, many of our clients prefer to roll those old 401(k) accounts into their current account to make sure it is managed for them, instead of having to figure out where and what to invest in themselves. Often times they are nearing or already past the capped fee we charge, so there is little to no financial benefit to us, but a big one for our clients.

Read MoreBeManaged February Newsletter – Do January’s Declines Portend the Rest of 2010?

Here are some of the topics discussed in this month’s newsletter from John Whaley, CFA, AIF, the director of our Research Department.

Do Late January Declines Portend the Rest of 2010?

Remember “Earnings Not as Bad as We Thought?”

Contributions Never More Critical Than Today

What Companies and Industries are in Your Portfolio?

Why Is Your 401(k) In Trouble? Because You Don’t Have Time To Read This Post

Our lives are as busy as ever. Family, school activities, committees, church, associations…oh, and that job thing too. These are the days of never really “disconnecting” with laptops, netbooks and smart phones constantly keeping us informed and “connected.”

Additionally, the multitude of responsibilities we are responsible for continues to increase. Your 401(k)? Yeah, that’s one of them. Lack of time is the #1 response people give us when they sign up for our BeManaged or BeAdvised service.

Read More5 Dumb Investing Mistakes to Avoid

We don’t call anyone dumb, because when it comes to investing, really “smart” people make as many or more mistakes as investing novices. The underlying issue? Our behavior and choices, which are often misguided by emotions. Investment behavior’s impact on investors’ returns have been well documented over the past few years. This is evidenced by the book referenced in article below, Why Smart People Make Big Money Mistakes, as well as by our friends at BehaviorGap.com.

Read More401(k) Investors: Keep Retirement Planning Simple

The video below is a very concise, simple advice on planning for your retirement by focusing on the KISS principle: Keep It Simple Stupid (I have to remind myself of this all of the time).

Here are some key points covered to focus on:

Save – You are responsible for your own future, do not expect the market’s returns to bail you out.

Understand Yourself – Risk is critical, so if you don’t understand it (most don’t), get some help.

Don’t Chase Returns – It’s a “loser’s game” based on the emotional response we have with this strategy.