Posts Tagged ‘401k advice’

A Model for 401(k) Advice, Pt. 2 – Must be Ongoing

A fiduciary relationship is one which is ongoing, in which the fiduciary is responsible for conducting ongoing due diligence on the various provisions for which they are responsible. A company fiduciary is charged with the responsibility of ongoing due diligence of the various fees, investment options, and vendor capabilities of the plan for the benefit of the participants. An ERISA fiduciary, regardless of the “flavor,” is hired to provide ongoing advice to the employer specific to investment due diligence and advice, vendor benchmarking, etc. Both of these more traditional fiduciary roles are ongoing relationships. Why isn’t employee fiduciary advice?

Read More401(k) Investors’ Achilles Heel #2: Goal-Based Investing – Good or Bad?

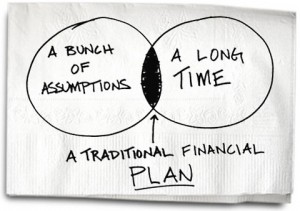

This month, our team has conducted dozens of 1-on-1 consultations. During these consultations, we walk the 401(k) investor through an investor questionnaire that takes into account their age, time horizon for accessing their 401(k) assets, and their risk tolerance. During this review of their account, we consistently run into investors who have an expectation of what they need to achieve from a performance standpoint in order to meet their goals. Just as I was considering this, Carl Richards wrote an article (click the napkin to read) specific to whether financial plans are worth the paper they are drawn up on.

Read More401(k) Investor Achilles Heel #1: Overconfidence

From time to time, all of us think we know what we are doing when clearly we do not, but it is not until we are proven wrong that we come to realize it. For me, it’s home repair. I know it’s not my strong suit, but my “man” button keeps blinding me to that fact until I am calling the repairman to fix the original problem and everything additional that I destroyed, broke, etc.

That, my friends, is humility. And humility is good for all of us. When it comes to investing, such overconfidence in our abilities can be extremely costly. In fact, the larger the balance of your 401(k), the more costly mistakes can be to you.

Read More18 Minutes on the New DoL 401(k) Advice Proposal

Our friend Jason Roberts, Partner at Reish and Reicher, has been closely monitoring the regulatory developments of 401(k) advice since the passage of the Pension Protection Act of ’06. The link below provides a brief, yet detailed overview of the regulations and what employers and advisors should take into consideration when it comes to the advice 401(k) investors receive. It is definitely worth the time.

Read MoreNew on LinkedIn: The 401(k) Fiduciary Advice Group

LinkedIn has been something I have been active on for over two years. It’s Groups feature has helped it evolve into a resource in which busy professionals can learn or get free guidance and feedback on various topics of interest. Personally, our company has benefited from other’s experience and expertise to the tune of saving thousands of dollars on various projects.

That being said, with the recent developments in 401(k) advice, we decided to create a group to help keep employers and advisors apprised of the regulatory and market developments that result from the clarifications. We launched the 401(k) Fiduciary Advice Group on Wednesday morning, and since then, there have been over 70 employers and 401(k) industry professionals join. Interested? Simply click the link below to join.

Read MoreBeManaged March ’10 Newsletter – The Advancing US Dollar and Your 401(k)

The following are some of the topics discussed in this month’s newsletter from John Whaley, CFA, AIF, the Director of our Research Department.

Advancing US Dollar Translates to Declining Foreign Stock Returns

Mutual Fund Fees and the Impact on Your Acccount

How Does Your 401(k) Account Growth Compare?

Brokers Win, Investors Lose Key Reform – WSJ

Every investor working with a financial planner/wealth manager/financial advisor/stockbroker…whatever title is used…should read at least the following quote. In Jason Zwieg’s article on WSJ.com, he provides one of the easiest to understand summaries I have read on the responsibility that person has to you:

As of now, the roughly 630,000 brokers, bankers and insurance agents registered to sell securities must determine whether investments are “suitable”—based on how wealthy you are, what else you have invested in, your tax status and your investment objectives.

Securities salespeople generally aren’t obligated to act in your best interest. They needn’t tell you that they make extra money pushing one particular investment or that cheaper alternatives might provide you a higher return.

Suppose two mutual funds are “suitable,” but one of them pays the broker a fatter fee. You may well end up in that one—without finding out that your broker had an incentive to favor it.

On the other hand, financial advisers—who are regulated as “fiduciaries” under the federal Investment Advisers Act—are obligated to put you first. They must explain their fees, disclose conflicts of interest and disclose past infractions. If they get paid extra to recommend a fund or sell an insurance product, they have to tell you.

Read MoreNew 401(k) Advice Proposal Available for Comments Until May 5th

As promised, the new 401(k) advice proposal has been delivered before the end of the month. While I admit to not having read it in its entirety, the following has been reported by the Wall Street Journal:

Read MoreA Model for 401(k) Advice, Pt. 1 – Must be Conflict-Free

Many 401(k) sponsors, providers and advisors eagerly await the DoL’s new advice proposal, which is due to be released within the next 30-45 days. In an effort to put in our two cents, we thought we would share our hopes for the proposal based on our experience in delivering advice, our understanding of other options in the marketplace, and the feedback we have received from employers and investors alike. Keep in mind most of our clients exist in the top end of the small market (250+ employees) to large sized employers (1,000+ employees).

Goal #1 – Advice Must be 100% Conflict-Free

We believe advice for 401(k) investors must be start with being conflict-free. If there are conflicts in providing participants advice, then 401(k) advice is doomed to fail. So, let’s look at how to ensure this holds true for participants and the employers that are required to do their due diligence on service providers, including advice providers.

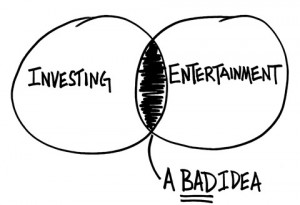

Investing Is Not Entertainment

As you know, we are big fans of the BehaviorGap. Our friend Carl Richards is now being featured in the New York Times website. His latest post there is two minutes of really good advice.

Am I investing to meet my most important financial goals or am I investing as a form of entertainment? For almost all of us, it can’t be both.